The latest limitation includes all of the outstanding expense you have, eg auto loans, unsecured loans and you will bank card balances

- Pay attention to the qualification standards and you will cost prior to getting a second possessions.

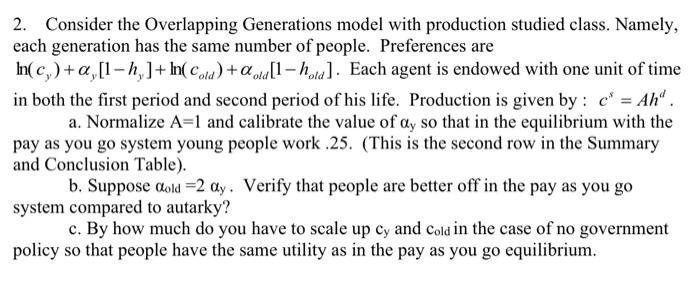

- The fresh new previous escalation in Most Customer’s Stamp Responsibility (ABSD) means you’d you desire way more cash when purchasing one minute house.

- To buy the second property comes with so much more financial obligations; its advised is clear regarding the purpose for buying the second property

Which have rising cost of living dominating statements into the previous days, rates are set to rise next regarding the upcoming days. If you have started attending and acquire the second possessions, this might be an enjoyable experience to begin with looking as the a beneficial rise in rate of interest could possibly indicate stabilisation out of assets costs.

Other than the cost of the house or property, there are lots of some thing might should be attentive to whenever to find a moment domestic, for example qualification, affordability and you may intent.

Qualifications

If you very own a private property, then you will be liberated to buy a moment private possessions without the court implications. not, whether your first property is a community property, should it be a setup-to-Order (BTO) apartment, selling HDB flat, executive condominium (EC), or Design, Make and sell System (DBSS) flats, then you’ll definitely need certainly to complete specific standards prior to you buy.

HDB flats have a good 5-seasons Minimum Occupation Months (MOP) requisite, meaning that you would must invade you to definitely property getting a great the least five years before you can offer or rent their flat. Additionally, you will need to complete the newest MOP until the payday loans Hartford pick out-of a personal property.

Carry out keep in mind that simply Singapore customers should be able to individual each other an HDB and a private property meanwhile. Singapore Long lasting Residents (PRs) will need to get-out of the flat in this half a year of one’s personal assets purchase.

Value

Residential properties are recognized to getting notoriously high priced in the Singapore and you can careful computations have to be built to ensure that your 2nd property purchase stays reasonable to you personally. You’ll have to take notice of one’s following the:

You might have to pay ABSD when you get one minute residential property. The total amount you’ll have to pay relies on their profile.

The fresh ABSD are past adjusted towards as an element of strategies in order to render a renewable assets markets. Newest cost is shown on table less than:

Considering the current ABSD prices, an effective Singapore Citizen just who already is the owner of an enthusiastic HDB apartment however, wishes to buy a personal condominium charging $1 million must fork out an ABSD of $2 hundred,000 (20%). Create observe that so it count is found on top of the client’s stamp responsibility.

Your first domestic buy need just up to 5% bucks down payment for many who used a bank loan, your next possessions requires a twenty-five% bucks advance payment of your property’s valuation maximum. Considering a home that’s appreciated on $1 million, you’ll you prefer $250,000 bucks to possess down payment.

The Debt Repair Proportion (TDSR) construction was introduced on to avoid home buyers from borrowing from the bank as well much to invest in the acquisition off a home. Within the build, home buyers can only use to up 55% (modified toward ) of its disgusting month-to-month earnings.

When you yourself have a mortgage associated with your first property get, it can considerably affect the amount you could acquire for the 2nd family. Yet not, when you yourself have currently removed the mortgage in your earliest house, then you’ll just need to make sure that your monthly casing mortgage payments and some other month-to-month bills do not go beyond 55% of one’s monthly earnings.

For your earliest homes mortgage, you are permitted acquire doing 75% of the property well worth if you are using up a bank loan otherwise 55% in case the loan tenure is over thirty years or offers prior many years 65. For your next casing loan, the loan-to-well worth (LTV) ratio falls so you can forty-five% to own loan tenures up to 30 years. If your financing tenure exceeds twenty five years or their 65th birthday, your LTV drops to 30%.

Perhaps you have realized, to get a second possessions whenever you are however purchasing the borrowed funds out of very first household will want significantly more bucks. Centered on a home valuation out of $1 million, you will probably you desire:

While it’s you can to use their Central Provident Finance (CPF) to find another assets, when you yourself have currently made use of their CPF to you personally first house, you could potentially only use the excess CPF Average Membership savings getting your next property just after putting aside the present day Earliest Old-age System (BRS) off $96,000.

Purpose

To order an extra property boasts far more economic obligation than the very first you to definitely, and is advised become obvious regarding the mission getting buying the 2nd possessions. Would it be for funding, or are you currently using it just like the the second domestic?

Clarifying your own objective will help you to for making specific decisions, including the sort of property, as well as choosing a location that would finest fit their mission. It is especially important should your next home is a financial investment possessions.

Like any other opportunities, you’d need work-out the potential rental yield and you can financial support really love, plus determine the projected profits on return. As a property purchase is an enormous money, it’s also wise to possess a method you to believe factors like:

What exactly is disregard the panorama? Might you make an effort to bring in a return shortly after five years, or even retain they toward a lot of time-identity to gather book?

Whenever as well as how do you really clipped loss, if any? Whether your mortgage repayments was higher than the lower leasing income, how much time do you really hang on ahead of offering it off?

To find a house within the Singapore try financing-extreme and buying another domestic will demand far more economic wisdom. One miscalculation might have high monetary outcomes. As a result, created an obvious plan and you can demand a wealth considered director to with you are able to blind spots.

Initiate Believed Now

Here are some DBS MyHome to sort out new figures and get a house that suits your finances and tastes. The good thing it slices out of the guesswork.

Rather, prepare having an out in-Principle Acceptance (IPA), so that you possess certainty precisely how far you might borrow having your house, enabling you to understand your budget precisely.